From current rates on nominal and real bonds, we can infer expected real interest and inflation rates. Markets anticipate that real interest rates will remain slightly higher than 2% for the foreseeable future. They also expect inflation to exceed the 2% target for the next 20 years. The latter poses a challenge for central banks.

In my last analysis (link), I demonstrated how to calculate implied forward rates from interest rates (yields) on bonds of varying maturities. According to the Expectation Theory of Interest Rates, these implied forward rates represent the market’s best estimate of future interest rates. I illustrated that the market anticipates future interest rates to be like current ones. Presently, 10-year US nominal interest rates (10-year Treasuries) are around 4.5%, and the market expects them to remain around 4.5% in both 2034 and 2044. However, I also highlighted that these implied forward rates are generally poor predictors of actual future interest rates.

Regardless of whether one believes that market-implied forward rates are accurate predictors of future interest rates, it remains intriguing to see what the market anticipates. Therefore, we can perform the same type of calculations for other interest rates, such as those on inflation-indexed bonds, i.e., real interest rates. This would allow us to determine the market’s best estimate of future real interest rates. With expected nominal rates and expected real rates, we can then calculate expected inflation rates.

Market-implied future real interest rates

By following a similar calculation method as in my previous analysis, but applying it to inflation-indexed bonds, we can determine expected real interest rates. Figure 1 presents the results of such calculations for the US since 2005.

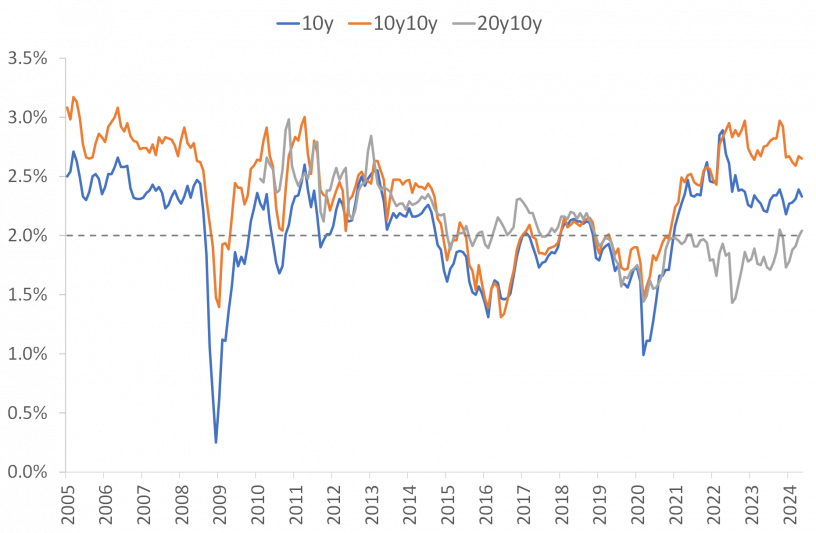

Figure 1. Yield on ten-year Inflation-Indexed Treasuries (10y), ten-year forward real interest rates in ten years (10y10y) and ten-year forward real rates in twenty years (20y10y). 2005–May 2024, though 20y10y for 2010–May 2024. Data source: St. Louis FRED and J. Rangvid.

Figure 1 shows the time-series movements in current 10-year real interest rates, expected 10-year real interest rates in 10 years (10y10y), and expected 10-year real interest rates in 20 years (20y10y). As with nominal interest rates, as presented in my last analysis, investors expect future real interest rates to be roughly equal to today’s real interest rate. More precisely:

- The 10-year real interest rate today (month of May 2024) is 2.15%.

- Markets expect the 10-year real interest rate to be 2.29% in ten years, i.e., in 2034.

- The expected 10-year real interest rate in twenty years, i.e., in 2044, is 2.40%.

While the conclusion is that markets do not expect any significant changes to real interest rates over the next 30 years, this (constant real rates) has not always been the case. For instance, during and immediately after the pandemic, the real 10-year interest rate was negative at -1%, as shown in Figure 1. This means that if you bought a 10-year inflation-indexed bond in 2020 and held it until maturity, it would provide you with a negative real return of minus one percent every year over the next ten years.

Investors did not expect such negative real interest rates to persist, however. During the pandemic in 2020, the 10y10y rate was close to 0%, while, as mentioned, the 10y rate was at -1%. This means that investors expected a -1% negative annual return from 2020-2030, but a higher return (zero percent) over the ten-year period starting ten years from then, i.e., over the 2030-2040 period. Additionally, during the pandemic, investors expected a real return of around 0% during the 2040-2050 period, as indicated by the 20y10y real yield hovering around 0% in 2020.

Alongside the rise in nominal interest rates and inflation since 2021, real rates and expected future real rates have also risen. Today, as mentioned, an inflation-indexed bond will provide slightly more than a 2% real return over the next ten years, and the same is expected over the 2034-2044 period and over the 2044-2054 period.

Expected inflation

In my last analysis, I calculated expected nominal interest rates. Above, we have calculated expected real interest rates. By subtracting the latter from the former, we can determine expected inflation rates (excluding the effects of risk premiums).

Figure 2 illustrates the results of this calculation, showing the expected annual inflation rate over the next 10 years (10y), the expected annual inflation rate for the period from 2034 to 2044 (10y10y), and the expected annual inflation rate for the period from 2044 to 2054 (20y10y).

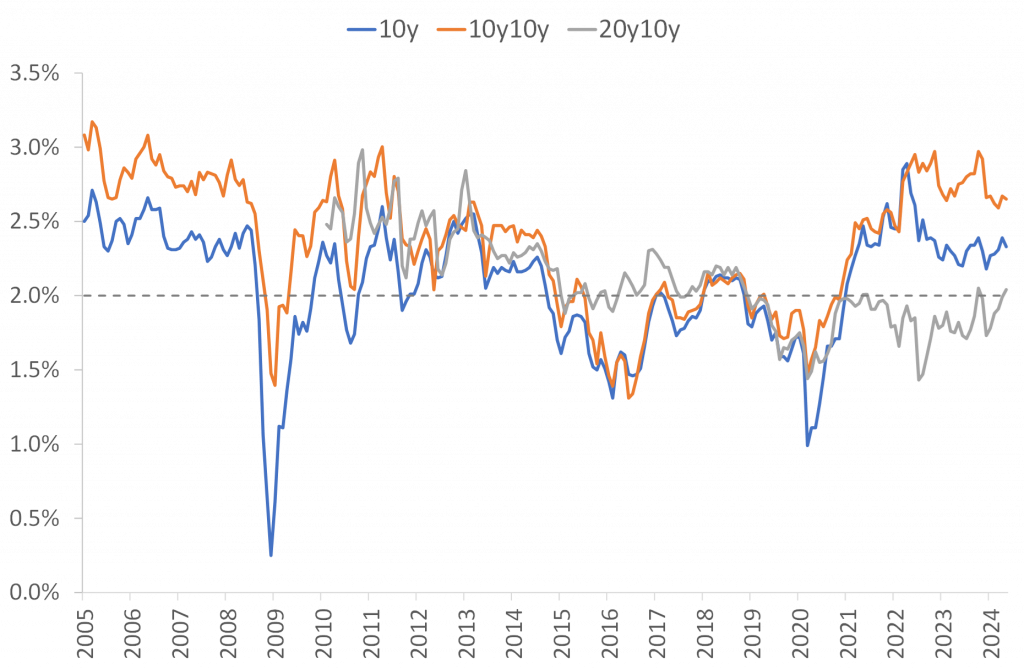

Figure 2. Expected inflation over the next ten years (10y), over the next ten years, ten years from now (10y10y) and over the next ten years, twenty years from now (20y10y). 2% target indicated by dashed line.2005–May 2024, though 20y10y for 2010–May 2024. Data source: St. Louis FRED and J. Rangvid.

Figure 2 reveals an interesting development in expected inflation following the inflation flare-up in 2021. Up until the pandemic, inflation and expected future inflation closely tracked each other. However, after the pandemic and the associated inflation surge, expected inflation over the next ten and twenty years is considerably higher than expected inflation twenty years out. Investors anticipate that inflation will be slightly above the Fed’s 2% target over the next ten years (2024-2034), at 2.33% per year. They expect inflation to be even higher, averaging 2.65% per year, for the 2034-2044 period.

The Fed’s inflation target is 2%. When investors expect annual inflation of 2.3% for 2024-2034 and 2.65% for 2034-2044, it suggests that they believe the Fed will struggle to control inflation for the next twenty years. Only twenty years from now do investors expect inflation to align with the 2% target.

You might argue that 2.3% and 2.65% are not much higher than the inflation target of 2%. I do not think the Fed agrees. I think the Fed would like expectations to be closer to 2% .

Interestingly, long-term (20y10y) inflation expectations have remained relatively constant at around 2% before, during, and after the inflation outbreak. This indicates that investors have strong confidence that the Fed will eventually manage to control inflation, although they believe it will take up many years to achieve this.

Another notable feature from Figure 2 is that investors significantly revise their expectations downwards during economic crises. During the global financial crisis of 2008, investors expected inflation to barely exceed 0% over the following 2008-2018 decade. A similar pattern occurred during the pandemic. In 2020, investors expected 1% inflation over the 2020-2030 period. Simultaneously, they expected inflation to be at target (2%) in the long term, as the 20y10y inflation expectations remained around 2% during these recessions.

Conclusion

Investors expect inflation to remain above the Fed’s 2% target over the next twenty years, only returning to target after 2044. This is not good news for the Fed, as they aim to anchor them around the inflation target. Whether inflation expectations then accurately predict future inflation is another matter.