Inflation, Inflation expectations, Real interest rates

Markets think inflation will be too high for the next 20 years

Don’t rely (too much) on implied forward rates when predicting future interest rates

Money and inflation

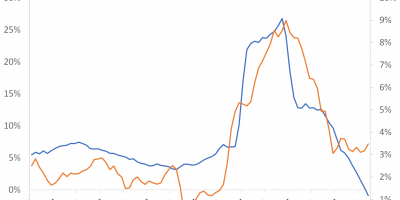

Danish economy, Exchange rates, Monetary policy

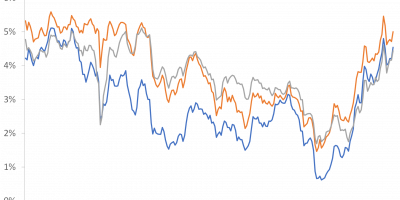

Do monetary policy regimes matter? Evidence from the Nordics

A solution to Larry Fink’s pension problem can be found in Denmark

Central banks, Inflation, Interest rates, Monetary policy

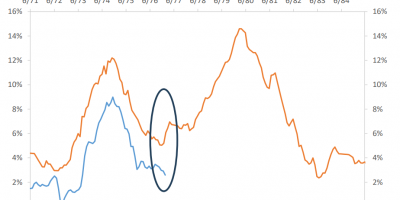

Monetary policy in the 1970s and today

Interesting papers, Stock markets

Magnificent 7. Or is it Magnificent 2?

Interest rates, Interesting papers, Return expectations, Stock markets

The expensive stock market

Central banks, Inflation, Inflation expectations, Monetary policy