There are similarities between Greece in 2010 and Italy today that make me nervous.

Do you remember the Greek drama in 2010-2012? Following the financial crisis in 2008-2009, Greece saw it public finances deteriorate, as did most other countries. The special thing about Greece was that they had fudged the numbers. In autumn 2009, the new Greek Prime Minister, George A. Papandreou revealed that the former government had lied about the deficit. This, and the recession, brought public debt to 146% of GDP in 2010. It later turned out that Greece had also falsified the numbers – via different swap contracts, willingly helped by US banks – prior to the introduction of the euro, making the whole thing even worse. With debt running at close to 150% of GDP in 2010, investors lost faith. Greek yields skyrocketed (see below). Greece received a number of rescue packages from the EU commission, IMF, and the ECB (the so-called “Troika”). Eventually, in 2012, Greece restructured its debt in the largest sovereign default in history. Investors faced a loss to the tune of EUR 100bn.

Why do I repeat this sad story? Because the IMF Fiscal Monitor Report contained a forecast for Italy that has, in my opinion, not received enough attention. The IMF predicts that Italy will reach a public debt level of 150% of GDP this year, exactly like Greece in 2010. Will this lead to a replay of the European debt drama?

First, the data. We are in the middle of a terrible recession. Italy has been severely affected by the corona virus, and has as a consequence enforced a strict lockdown. IMF expects that Italy will be one of the worst hit countries. Italian GDP is expected to fall by 9.1% during 2020.

IMF also expects that the fiscal deficit will be 8.3% of GDP in 2020. This is a large deficit, but other countries face even larger ones. The US, for instance, 15.4% of GDP (this probably requires another blog post…..), China 11.2%, Spain 9.5%, and so on.

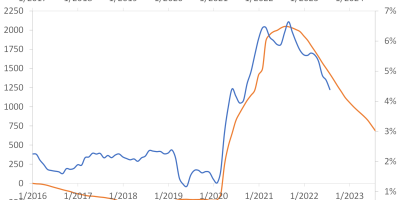

The problem in Italy is that public debt levels are already very high, at 130% of GDP. Few countries match this. In fact, only Japan and Greece. What is noteworthy, in my opinion, is that the combination of the already high debt level, the severe recession, and the fiscal deficit will most likely take the debt level to more than 150% in 2020:

Data source: EU Open Data Portal and IMF Fiscal Monitor Report.

The figure superimposes a dotted line indicating the 146% debt-to-GDP level Greece reached in 2010, which sparked the Greek problems. Italy is expected to cross this line in 2020.

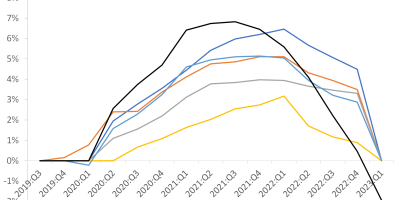

Contributing to my concern is the fact that financial markets seem to treat Italy and Greece somewhat similar this time around, in contrast to 2010. This time, movements in the Italian yield spread to Germany largely mirror movements in the Greek yield spread:

Data source: Thomos Reuter Datastream via Eikon.

The spread between Greek and German ten-year government bonds is a little higher than the spread between Italian and German government bonds, but movements are very similar. Only between the ECB/Christine Lagarde blunder on March 12 and the introduction of the PEPP (see below) on March 18, there was some divergence between Italian and Greek yields. Otherwise, they have moved in tandem.

This is different from 2010. In 2010, Greek yields spiraled out of control, reaching close to 50% on the worst days, but something like 25% for the worst month on average:

Data source: St. Louis Fed.

The Italian spread also increased in 2010, but, back then, markets clearly distinguished between Greece and Italy. Today, markets view Italy and Greece as being in somewhat similar situations. Rating agencies have started to act (Link).

Will we see a repetition of the Greek drama?

The Greek yield spread was close to 50% on the worst days in 2010, and currently we are talking something like 2.5% for Italy, i.e. very far from 50%, though up from 1.5% in the beginning of the year. This is clearly not as bad as in 2010. I thus hope that we will not see a repetition of the Greek story in Italy, but I dare not rule it out.

Let us start with the good news. Yields are lower today than in 2010. In 2010, Italian yields were around 4%. Today, they are around 2%. Hence, if yields stay low, Italy can afford a larger public debt compared to the situation in 2010. Also, everybody is aware that problems in Italy will mean problems for Europe, as I describe below, i.e. everybody wants to avoid such a situation.

On the other hand, the situation could turn to the worse if the recession in Italy will be deeper than the IMF expects, if the Italian political situation takes another turn to the extreme, if political negotiations at the EU level about a recovering plan do not bear fruit, or if some other negative shock occurs. Should some of this happen, Italy might find itself in something like the Greek situation at some point. The situation is fragile, as shown by the widening of spreads and the downgrade of Italy.

Italy is important for the European project. It is a G7 country. It is one of the founders of the EU. The foundation of the euro would be threatened if Italy runs into trouble. It would have global repercussions. At the same time, Italy is probably too big to bail out for the rest of the Eurozone/EU.

Some say that the ECB will make sure that this will not happen. Perhaps, but this is not as obvious as some claim. We get into technical nitty-gritties here, unfortunately, but it is important to understand.

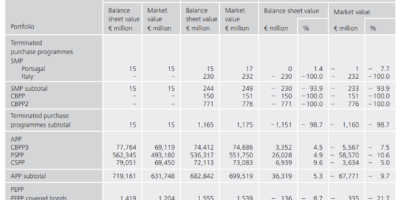

ECB is buying bonds like crazy at the moment, keeping a lid on yields, including Italian. The ECB’s PEPP (Pandemic emergency purchase programme) implies that the ECB will buy public and private securities to the tune of EUR 750bn during 2020. I.e., the PEPP will help keeping Italian yields down.

Furthermore, at the ECB Governing Council meeting Thursday, April 30, it was decided that “The Governing Council will conduct net asset purchases under the PEPP until it judges that the coronavirus crisis phase is over, but in any case until the end of this year” and “The Governing Council is fully prepared to increase the size of the PEPP and adjust its composition, by as much as necessary and for as long as needed”. Hence, the PEPP might last longer than throughout 2020 and accumulate to more than EUR 750 bn.

BUT, the important sentence in the PEPP programme is this one: “For the purchases of public sector securities under the PEPP, the benchmark allocation across jurisdictions will be the capital key of the national central banks. At the same time, purchases will be conducted in a flexible manner. This allows for fluctuations in the distribution of purchase flows over time, across asset classes and among jurisdictions.” (Link).

This point here is that that ECB cannot – and I repeat cannot – buy unlimited amounts of Italian debt at the moment. The proportion of Italian bonds the ECB can buy (as a proportion of all Eurozone sovereign debt ECB buys) is restricted by the Italian fraction of ECB capital. At the moment, this is, to be very precise, 13.9165%.

It also says that this will be interpreted in a “flexible manner” – and I am sure the ECB will be flexible – but they cannot be too flexible. ECB just cannot buy unlimited amounts of Italian debt under current programmes.

There is an escape clause: OMT (sorry for this soup of abbreviations; ECB, PEPP, OMT,…). OMT is “Outright Monetary Transactions”. OMT allows ECB to buy unlimited amounts of Italian (and other Eurozone) bonds, should this be necessary. But, and this is a big but, only when the relevant country has entered into a program with the European Stability Mechanism (ESM; one more abbreviation…). An ESM program means that the country will face demands with respect to its conduct of fiscal policy; think about the discussions about the role of the Troika in the Greek drama. To some extent, this is a loss of sovereignty. Entering into a program is also a signal that the country cannot handle the situation on its own. This will make it even more difficult to sell bonds on the market. At the moment, Italy very clearly opposes an ESM program. At the end of the day, this however means that ECB cannot buy unlimited amounts of Italian debt should this become necessary. ECB cannot save Italy.

Other people say “look at Japan”. Japan has a public debt of more than 200% of GDP. IMF expects it to reach 252% of GDP in 2020. Yields in Japan are very low, in spite of this massive debt mountain. I.e., Japan shows that you can accumulate lots of public debt without causing yields to rise, some claim. True, but remember that Japan has its own currency and its own central bank. The Japanese central bank can buy all the public debt they want, keeping Japanese yields down. Italy does not have its own central bank and its own currency. The ECB cannot buy unlimited amounts of Italian bonds. Greece is the example that shows that the situation of a Eurozone country is different from the situation of a country with its own currency and central bank.

(Here, I do not want to get into a discussion whether a country with its own currency and central bank faces no limits on the amounts of public debt it can raise, as argued by proponents of the “Modern Monetary Theory”. Basically, I disagree with that policy implication and think there is a limit, but this is for another day).

So, in the end, if worst comes to worst, ECB cannot save Italy, unless Italy enters into an ESM program. Some kind of political solution at the EU level would be needed. I hope we will not get there. At the moment, we are not, but I dare not rule that we might get there. I will follow the Italian situation.