What is the relation between economic activity and the stock market over the business cycle? This blog post presents some of the conclusions from my book From Main Street to Wall Street. One conclusion is that the business cycle has a strong impact on the stock market, another that post-1945 business-cycle dynamics are very different from pre-1945 business-cycle dynamics.

In this third part of my small four-part series of blog posts presenting glimpses of my book From Main Street to Wall Street, I turn to its examination of the relation between the stock market and the economy over the business cycle. It follows my first post (link), where I explained why I wrote the book, and the second (link), where I presented some of the book’s conclusions with respect to the long-run relation between the stock market and the economy.

The business cycle

In this part of the book, I explain what the business cycle is, what characterizes it, what causes business-cycle fluctuations in economic activity, and economic theories that explain business cycles.

Business-cycle fluctuations refer to common fluctuations in a large number of time series measuring business activities. The business cycle consists of different phases, called expansions and contractions/recessions. Business-cycle dynamics are recurrent alternations between expansions and contractions.

A common rule of thumb is that the economy is in recession when GDP has fallen for two consecutive quarters. Some countries, in particular the US, do not use this rule-of-thumb but rely on committees that determine turning points in economic activity. In the US, for instance, the “NBER Business Cycle Dating Committee” (link) determines when the US economy contracts and expands.

One of the exiting conclusions in this part of the book is that recessions were more frequent, and expansions consequently shorter, before the Second World War. Or, in other words, Advanced Economies have experienced fewer and shorter recessions since the Second World War. This is obviously a good thing, as recessions cause unemployment, falling incomes, and other experiences we would like to avoid.

Figure 1 shows the length of each expansion in the US economy since 1871 (in number of months):

Source: © From Main Street to Wall Street.

The figure shows that, since 1945, the average expansion lasts longer. An interesting statistic that the book presents is that, on average, the US economy was in recession in four out of ten months before 1945. After 1945, the US economy has been in recession in less than two out of ten months. Recessions have become rarer since the Second World War.

In the book, I discuss how we have achieved this important and welfare-improving change in the behaviour of economic activity.

The stock market over the business cycle

A main conclusion in my previous post (link) was that there is a weak relation between economic growth and stock returns in the long run. (Remember here to distinguish between stock prices and stock returns: there is a weak relation between stock returns and economic growth but some relation between stock-price growth and economic growth).

This conclusion is dramatically different when talking about the business cycle. Over the business cycle, there is a strong relation between economic growth and economic activity. Stock returns are low during recessions and high during expansions. This is an important conclusion to recognize for academics who build models to understand the drivers of stock returns and for investors.

It is true that the stock market is considerably more volatile than economic activity, as I return to in my final blog post in this series. For example, legandary economist Paul Samuelson (the first American to win the Nobel Prize in Economics) famously joked that ‘the stock market has predicted nine out of the last five recessions’, i.e. the stock market tanks more often than does economic activity. Still, on average, stock returns are considerably higher during expansions. In the book, I show that the US stock market has returned around 10% per year on average during expansions (since 1871) in real terms. During recessions, the average real stock return is negative, at -1.2%. This is a very large difference. I illustrate the consequences in Figure 2 below.

I also investigate bond returns. Due to the fact that central banks lower monetary policy rates during recessions, bonds typically provide positive returns during recessions; lower interest rates cause higher bond prices, and thus positive returns from bonds. This is particularly true since 1945, as central banks have been more active in influencing the business cycle after 1945.

Figure 2 illustrates the importance of accounting for the differences in returns across expansions and recessions. I calculate the return investors would have obtained if they had been able to perfectly time the market. I should stress that nobody is able to perfectly time the market, i.e. this calculation serves as an illustration of the importance of the business cycle.

I consider three types of investors. First, a fantastic investor. This hypothetical fantastic investor invests in stocks during expansions and bonds during recessions. I compare the cumulative return of this investor to the return another investor would have obtained if he/she was invested in the stock market all the time. Finally, I compare it to the return of an investor who was invested in the stock market during recessions and the bond market during expansions. This last investor is a disastrous investor. I calculate the cumulative returns of the three strategies, assuming that they all invested USD 1 in the stock market in 1871. The results of these calculations are in Figure 2.

Source: © From Main Street to Wall Street.

The investor who was always invested in the stock market would have seen his/her USD 1 grow to app. USD 17,000 in 2018. This is the cumulative real return of the US stock market over 150 years. This is a fantastic return. If one had been able to avoid recessions, it would have been even better, though.

Consider our hypothetical fantastic investor. The hypothetical investor who was able to perfectly time the market, i.e. invest in the stock market during expansions, sell out before a recession arrives, invest the proceeds in the bond market during recessions, only to return to the stock market at the start of the next expansion, would have seen his/her USD 1 grown to app. USD 90,000 in 2018. This is of course marvelous. It is five times more than the already impressive cumulative return of the overall US stock market.

The fact that the return to the perfect market timer is so much higher than the return to the investor who was invested in the stock market during all periods shows that recessions hurt stocks. It would be so much nicer if one was able to avoid the stock market during recessions but reap the benefits during expansions. In the real world, nobody is able to perfectly time the market, but Figure 2 reveals the importance of the business cycle for the stock market.

Finally, consider the return to the disatourous investor. This is the investor who was perfectly bad at timing the market. This investor invested in stocks during recessions and bonds during expansions. It is a catastrophic investment strategy. This investor would end out with less than USD 1 in 2018. In other words, the investor would not have obtained any real return over 150 years. The conclusion is that the business cycle heavily affects financial markets and returns. It emphasizes the importance of understanding the underlying economy when trying to understand the stock market, which is the goal of the book.

I show in the final part of the book (that I turn to in the next blog post) that it is difficult to forecast recessions and expansions. Consequently, it is difficult to time market entries and exits perfectly. The point of Figure 2, thus, is to illustrate the importance of the business cycle for the returns we obtain, not to say this is something anybody can obtain.

Interest rates during the business cycle

To understand business cycles, one needs to understand central banks. Central banks lower monetary policy interest rates during recessions, in order to get the economy going and boost inflation, and increase policy rates during economic booms, in order to contain inflationary pressures. I explain what central banks are, how they conduct monetary policy, what monetary policy goals and instruments are, the transmission mechanism, etc.

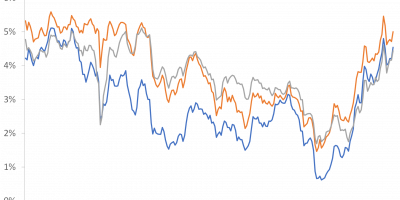

I show that monetary policy influences the shape of the yield curve, i.e. the relationship between yields on bonds of different maturities. Typically, central banks increase the monetary policy rate during late phases of expansions, and decrease policy rates during early phases of recessions. The monetary policy rate is a short-term interest rate. Long-term interest rates are more persistent. Hence, the yield curve flattens before recessions, only to increase during recessions, as Figure 3 shows.

Source: © From Main Street to Wall Street.

As an example, consider what happened before the financial crisis. Start in, e.g., 2004, i.e. a couple of years before the financial crisis of 2008. Yields on ten-year Treasury Bonds were 3-4 percentage points higher than the Fed Funds Rate, the monetary policy rate of the US central bank. In 2004, the Fed started tightening monetary policy, i.e. increased the Fed Funds Rate. The difference between long- and short-term yields dropped. The yield curve flattened. This lasted until the beginning of the recession in 2007, when the Fed slashed the policy rate, increasing the slope of the yield curve again. Figure 3 reveals that this is a systematic pattern. Yield curves flatten before recessions only to increase during recessions.

When it is a systematic pattern, it indicates that we might be able to use the slope of the yield curve to forecast recessions. This is something I describe in the last part of the book that deals with forecasting economic activity and stock returns.

I also describe the financial crisis of 2008 in this part of the book. I do so to give an example of how a business cycle develops. I describe the economic expansion before the financial crisis, what caused it, and how policymakers reacted. I also describe how the stock market behaved before, during, and after the financial crisis. This chapter of the book thus gives a more detailed account of what causes business cycle fluctuations, illustrated by one fascinating episode, i.e. a kind of “case study”. This chapter builds upon the work we did in the committee that investigated the causes and consequences of the financial crisis in Denmark, the so-called Rangvid-committee (link).

Conclusion

Economic activity fluctuates around the long-term growth trend. During expansions, economic growth is high. During recessions, the economy contracts.

Business cycles are important for financial markets. The stock market is volatile, but typically does well when the economy is doing well. On the other hand, the stock market typically tanks during recessions. Understanding how the business cycle affects markets is important for investors and academics.

Knowledge about the historical relation between economic activity and financial markets should help us when formulating expectations to future returns. I deal with this in my next and final part of this series of blog posts describing From Wall Street to Main Street.