The Magnificent 7, the seven US tech giants, accounted for most of the gains in the S&P 500 in 2023. However, this was against the backdrop of a terrible 2022 for Mag7. Over a longer period, since 2021 for instance, only two of the seven stocks have significantly outperformed the market. This illustrates a general point: past winners are usually not future winners.

Much has been written about the Magnificent 7, the seven US tech stocks (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) that dominated the US stock market in 2023.

I joined the debate last year (link, link) and concluded that Magnificent 7 generated most of the return of the S&P 500 in 2023. I showed that “only 7 out of 500 stocks generated 10.8%/15.3% = 71% of the return of the S&P 500 in 2023. The remaining 493 stocks delivered the remaining 29%.”

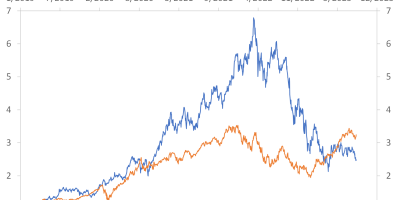

I also showed that this is not just a phenomenon of 2023. The Magnificent 7 have grown much faster than the other 493 stocks in the S&P 500 for many years, especially during the 2013-2021 period. In Figure 1, I show the combined market value of the Magnificent 7 stocks as a fraction of the combined market value of all 500 stocks in the S&P 500. Ten years ago, the Magnificent 7 represented about 7% of the total value of all 500 stocks in the index. Today, the weighting of these seven stocks is almost 30%.

Source: Datastream via Refinitiv and J. Rangvid.

Figure 1 also shows that the developments before and after – let’s say – 2021 were different. Before 2021, the Magnificent 7 (Mag7) rose faster than the rest of the market every year. Since 2021, it’s been more of a rollercoaster ride. The Mag7’s weight in the index rose from 24% at the start of 2021 to 28.5% today, but the ride has been choppy and less pronounced than before 2021.

This became particularly clear in 2022 and 2023. In 2022, Mag7 fell much more than the index, while in 2023, on the other hand, Mag7 rose much more than the index.

In figures, the total market value of all 500 stocks in the S&P 500 index fell by 20% in 2022, from USD 40.6 trillion to USD 32.1 trillion, while the value of the Magnificent 7 fell by 33%, from USD 10.7 trillion to USD 6.3 trillion. In 2023, on the other hand, the market grew by 24.6% and rose to USD 40 trillion at the end of 2023, while Mag7 increased by 76%(!) to USD 11 trillion.

So, yes, Magnificent 7 had a spectacular run in 2023, accounting for a large part of the index’s total gain, as I showed in my previous analyses (link, link). But that was against the backdrop of a horrendous 2022.

There is thus reason to reassess Magnificent 7’s performance, not just focusing on 2023, but taking a longer perspective, covering both 2022 and 2023 and more.

Heterogeneity among Mag7 stocks

Market opinion says that the Magnificent 7 dominate the market and are “great” stocks. But is that true? Maybe it’s not seven stocks that dominate the market anymore. Perhaps there are far fewer.

Look at Figure 2. The figure divides the Magnificent 7 into two groups and shows their weights in the index since 2021. One group consists of only two stocks: Microsoft and Nvidia. I call them “Mag2”, an abbreviation for the “Magnificent 2”. The other group consists of the remaining five stocks: Alphabet, Amazon, Apple, Meta and Tesla. I call them “5NSMA”, an acronym for “5 Not So Magnificent Anymore” stocks.

Source: Datastream via Refinitiv and J. Rangvid.

In 2021, the five Not-so-Magnificent-Anymore stocks accounted for 18% of the total value of all 500 stocks in the index. The Magnificent 2 (Microsoft and Nvidia) accounted for 6.3%. Since 2021, the 5NSMA have underperformed the index. Today, their weight in the index has fallen to 16.2%.

On the other hand, the Magnificent 2 have significantly outperformed the market. In 2021, Microsoft and Nvidia together accounted for the aforementioned 6.3% of the market. Today they account for 12.3%.

In addition, the 5NSMA had a truly terrible 2022, with their combined weight in the index falling from 18.7% at the beginning of 2022 to 12.8% at the end of 2022.

The Mag2 also underperformed in 2022, but not by as much. Their weight fell from 8% to 6.7%.

The conclusion is that over the last three years, five of the so-called Magnificent 7 are in fact not so magnificent. Together, these five stocks have underperformed the market. There are no longer seven magnificent stocks. There are two.

Positive returns but underperformance

Note that I’m not saying you didn’t make money on the 5NSMA stocks. You did. The total value of 5NSMA at the beginning of 2021 was USD 5.7 trillion. Today, it’s USD 7 trillion, an increase of 22.8%. So, what’s the fuss about?

The issue is that the other shares have also risen. And by more. The other 493 shares in the S&P 500 have risen from a total value of USD 23.9 trillion at the beginning of 2021 to USD 31.9 trillion today, an increase of 33.5%. This means that investors have raised the price they are willing to pay for other stocks more than the price they are willing to pay for the five not-so-great-anymore stocks. 5NSMA have underperformed since 2021. These five stocks were magnificent up until 2021, but have not been magnificent since then.

Picking stocks

Why is this important? Isn’t this just after-the-fact gobbledygook? It may seem so, but there is of course a reason for all this. Or rather two points.

Firstly, I hope to change the narrative. There are no longer seven great stocks. There are two. I think that’s important given the market narrative.

Secondly, this has implications for stock selection.

In my last analyses (link, link), I referred to the contributions of Professor Hendrik Bessembinder, who showed in academic research that most individual stocks underperform a risk-free investment.

But we always hear that equities outperform bonds, right? That’s true if you look at the overall stock market, but not the typical individual stock. The reason the overall stock market outperforms a risk-free investment, while the typical individual stock does not, is that a few stocks do spectacularly well, i.e. the large positive returns of a few stocks offset the small and often negative returns of the typical stock.

If you can identify these few spectacular stocks ex ante, you will be very rich. That’s why many people hold concentrated portfolios. They hope they can pick those few winners. An interesting article from last year shows that this – holding a concentrated portfolio – is usually not a good idea.

Petajisto (link) analyses how concentrated portfolios perform. A concentrated portfolio means that you only hold a few shares. Petajisto shows that the median stock performs 7.9% worse than the broad stock market index over ten years. In other words: If you hold the typical stock, that is the median stock (which is the stock where half of all other stocks in the stock market universe do better than that stock and half of all other stocks do worse), you will do worse than a portfolio consisting of all stocks. In short: if you hold a single stock, you will typically do worse than the stock market index.

But then you would argue, “I’m not holding the typical (median) stock – I’m trying to find the “winner””. But how are you going to do that? Many people do that by holding the winners of the past. If Nvidia has done well in recent years, it will probably continue to do well. Right?

Petajisto goes on to show that you usually underperform if you follow the strategy of holding past winners. If you hold a stock that has been among the top 20% performers over the last five years, the average ten-year return is 17.8% lower than the market. So, if you hold a stock that has been a winner in the past, it often underperforms the broader stock market. In 93% of all months since the Second World War, the performance of a past winner over the next ten years is below that of the market.

The lesson here is that you should hold a well-diversified portfolio and not overweight individual stocks. Then we can discuss whether you should hold 30-50 stocks, as some active mutual funds do to try to beat the market, or whether you should hold the entire universe, as with a passive mutual fund. That is a topic for another day. But it is not advisable to hold just one, two or a handful of stocks like the typical individual investor does, as co-authors and I found out in our research (link).

Conclusion

As you walk through the aisles, you may hear: The Magnificent 7 have done well, I’ll buy one of them to improve my performance.

Your answer should be: You can do that, but you will most likely do worse than a broad equity portfolio. Recent research shows that past winners rarely continue to be winners.

This is clear from recent data. Magnificent 7 had a fantastic run until 2021. Many people bought them in the hope that they would secure spectacular future returns. However, since 2021, only two (Microsoft and Nvidia) of the seven “magnificent” stocks have significantly outperformed the market. Perhaps we should characterise the remaining five stocks as “Not-So-Magnificent-Anymore”.

The conclusion is that most investors are advised to hold a broad portfolio and not try to find the one stock that will rise spectacularly. The latter strategy is usually not successful.