Facing a looming recession and financial market panics, the Fed intervened heavily in late-February/early-March, lowering the Fed Funds Rate to zero and expanding its balance sheet dramatically. In spite of this, markets kept on panicking. Then, suddenly, on March 23, everything changed. Stock markets started their rally. This was not because the Fed lowered the rate or expanded its asset purchases even further, nor because the economic data improved. What happened? The Fed made an announcement. Nothing else. It is a fascinating illustration of how expectations can change everything on financial markets.

Much has been written about the massive interventions of the Fed during February and early March. In my previous post (link), I list Fed interventions as one of the reasons why the stock market is back to pre-crisis highs. In this post, I dig one step deeper and explain the fascinating story of how the Fed said something and thereby rescued markets.

Asset purchases and rate reductions did not save markets in February/March

Let us start by illustrating how the actual Fed interventions (interest rate changes and asset purchases) did not save markets in March. The Fed lowered the (lower range of the) Fed Funds Target Range to 1% from 1.5% on March 2 and then again to 0% less than two weeks later, on March 14. At the same time, it bought Treasuries and mortgage-backed securities to the tune of USD 600bn per week. These interventions succeeded in lowering yields on government and mortgage-backed bonds, but did not cheer up stock markets.

This graph shows how Treasury yields came down significantly in February/March, by basically 1.5%-point (from close to 2% to close to 0.5%; I show yields on 10-year Treasuries in this graph), as a result of reductions in the policy rate (the Fed Funds Rate) and asset purchases by the Fed.

Source: Fed St. Louis Database

The graph also shows that the SP500 continued falling throughout February/March. In other words, the massive interventions by the Fed in late-February/early-March (and these interventions really were massive – buying for USD 600 bn per week and lowering rates to zero is indeed a massive intervention) did not convince stock markets that the situation was under control. And, remember, these were not minor stock-market adjustments. It was the fastest bear market ever (link).

What turned the tide?

On March 23, the SP500 reached its low of 2237, a drop of 31% compared to its January 1 value. Since then, everything has been turned upside down and markets have been cheering, as the above graph makes clear.

What happened on March 23? The Fed had its finest hour. It did not do anything. It merely said something. A true “Whatever it takes” moment.

As you remember, a “Whatever it takes” moment refers to the July 26, 2012 speech by then ECB-president Mario Draghi (link). The speech was given at the peak of the Eurozone debt crisis. The debt crisis pushed yields on Italian and Spanish sovereign bonds to unsustainable levels. Italy was too big to fail, but also too big to save. The pressure on Italy was a pressure on the Eurozone construction. Mario Draghi explained the situation and said the by-now famous words:

“But there is another message I want to tell you. Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.”

Investors understood that the ECB would be ready to buy sovereign bonds to save the Euro. Markets calmed down. Italian and Spanish yields fell. And this – and this is the point here – without the ECB actually intervening, i.e. without the ECB buying Italian or Spanish bonds. The announcement that the ECB would intervene was enough to calm down investors.

Why is this relevant here? Because on March 23 the Fed sent out a press release, announcing that:

“…the Federal Reserve is using its full range of authorities to provide powerful support for the flow of credit to American families and businesses.”

And, then, as one of the new features announced the:

“Establishment of two facilities to support credit to large employers – the Primary Market Corporate Credit Facility (PMCCF) for new bond and loan issuance and the Secondary Market Corporate Credit Facility (SMCCF) to provide liquidity for outstanding corporate bonds.”

This statement turned everything upside down. The important thing is that this turn of events happened without the Fed using any money at all. It was a “Whatever it takes” moment (though, perhaps not as Dirty-Harry dramatic as Mario Draghi’s “And believe me, it will be enough”): The Fed announced what they would do, investors believed the Fed, and markets started cheering. It is a prime example of how investor expectations influence financial markets.

What are the PMCCF and SMCCFs, why did the Fed announce them, and why were their effects so dramatic?

The lowering of the Fed Funds Rate and the purchasing of Treasuries succeeded in lowering yields on safe assets, such as Treasury bonds, as explained above, but did not lower yields on corporate bonds. In fact, during the turmoil in late-February/early-March, credit spreads (the spread between yields on corporate bonds and safe bonds) widened dramatically. When yields on corporate bonds rise, it becomes more expensive for corporations to finance their operations. And, when yields rise a lot, as in February/March, investors get nervous about the profitability and survival of firms.

This graphs shows how yields on both the least risky corporate bonds (Triple A) and speculative grade bonds (Single B) rose dramatically in relation to 3-month Treasury Bills, with yields on lower-rated bonds (Single-B) naturally rising more than yields on higher-rated (Triple-A) bonds.

Source: Fed St. Louis Database

The important point in the picture is that the spreads continued rising throughout late-February/March, in spite of the intensive interventions described above, i.e. in spite of Fed purchases of government and mortgage bonds. The Fed was happy that safe yields fell, but was concerned that credit spreads kept on rising. Volatility in corporate bonds markets also rose (link), making the whole thing even worse.

More or less all firms saw their funding costs increase, even when there were differences across firms in different industries, with firms in the Mining, Oil, and Gas, Arts and Entertainment, and Hotel and Restaurant sector hit the hardest, and firms in Retail and Utilities sectors less affected (link). The Fed became nervous because higher funding costs for firms affect firms negatively, causing them to cut jobs, reduce investments, etc.

The Fed decided to act. It announced on March 23 that it would launch two new programs, PMCCF and SMCCFs. The PMCCF is the ’Primary Market Corporate Credit Facility’ and the SMCCF the ’Secondary Market Corporate Credit Facility’. Primary markets are where firms initially sell their newly issued bonds. The PMCCF should thus ease the issuance of newly issued corporate bonds, i.e. help firms raise funds. Secondary markets are where bonds are traded afterwards, i.e. the SMCCF should ease the trading (liquidity) of already existing corporate bonds.

The effect on equity and credit markets of the announcement of the PMCCF and SMCCFs was immediate and spectacular. Immediately after the announcement, credit spreads narrowed (see, e.g., link, link, and link).

Interestingly, stock markets reacted immediately, too. The stock market, thus, did not react to the lowering of the Fed Funds Rate and the extensive expansion of the Fed balance sheet in late-February/early-March, but reacted strongly to the announcement that the Fed would buy corporate bonds on March 23.

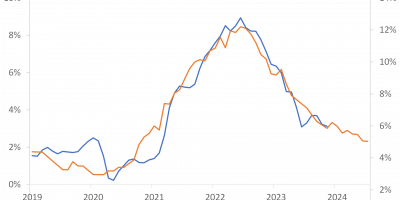

This (supercool, I think 🙂 ) graph shows developments on corporate bond and equity markets. The graph shows the spread between yields on AAA-rated corporate bonds and 3-month Treasury Bills and the stock market inverted, both normalized to one on January 1. The graph for the inverted stock market means that when the SP500 is at 1.45 on the y-axis on March 23, the stock price at January 1 was 45% higher than it was on March 23.

Source: Fed St. Louis Database

The parallel movements in equity and credit markets are striking. Equity and credit markets moved in parallel during January, when stock markets rose and credit spreads narrowed, in late-February/early-March when credit spreads widened dramatically and stock markets fell like a stone, as well as after March 23, when both credit spreads and stock markets improved spectacularly. Since then, stock markets have continued to rise and credit spreads have continued to narrow.

The correlation between the two series is an astonishing 0.93 for the January 2 through May 31 period.

The announcement effect

The Fed has experience with and a mandate to buy mortgage-backed securities and Treasuries. It had no such experience when it comes to purchases of corporate bonds and corporate bond ETFs. This means that the Fed could not start buying corporate bonds on March 23, it needed an institutional set-up. It created an SPV with capital injections from the Treasury and leverage from the New York Fed, it asked a financial firm (Blackrock) to help them purchase the bonds, etc. These things take time. The Fed only started buying corporate bond ETFs in mid-May and corporate bonds in mid-June.

Given that the Fed only started buying bonds and ETFs in May/June, the spectacular turnaround on March 23 really was due to the announcement only.

In slightly more detail, it played out as follows. The March 23 announcement primarily dealt with higher-rated corporate bonds (Investment Grade), and spreads narrowed immediately. On April 9, the Fed announced that they would expand “the size and scope of the Primary and Secondary Market Corporate Credit Facilities (PMCCF and SMCCF)”, buying bonds that were Investment Grade on March 22 but had been downgraded since then as well as corporate bond ETF. High-yield spreads tightened even more (link). Today, the Fed explains that the programs allow the Fed to buy “investment grade U.S. companies or certain U.S. companies that were investment grade as of March 22, 2020, and remain rated at least BB-/Ba3 rated at the time of purchase, as well as U.S.-listed exchange-traded funds whose investment objective is to provide broad exposure to the market for U.S. corporate bonds.”

The actual purchases began in May/June, several months after the announcement. Interestingly, the purchases themselves have had a modest impact only. First, the amounts of corporate bonds and corporate bond ETFs bought pale in comparison with the amounts of mortgage-backed securities (MBS) and Treasuries bought. The Fed has bought MBS and Treasuries to the tune of USD 3,000bn this year. It has “only” bought corporate bonds and ETFs for around USD 12bn. The amount used to buy corporate bonds thus corresponds to less than 0.5% of the amount used to buy MBS and Treasuries. This graphs shows the daily purchases. Using the latest figures from August 10, the Fed has basically stopped buying corporates.

Source: Fed webpage. Thanks to Fabrice Tourre for collecting and sharing the data.

So, the Fed has not bought a lot of corporate debt. It has, however, the power to buy a lot. The PMCCF and SMCCF set-up is such that the Treasury has committed to make an USD 75bn investment in the SPV that buys the assets (USD 50bn toward the PMCCF and USD 25bn toward the SMCCF). The New York Fed then has the ability to level this up by a factor of ten, i.e. the Fed can buy corporate debt for up to USD 750bn. This is a sizeable fraction of the total US corporate bond market. This, that the Fed can potentially buy a lot, helps making the program credible and thus helps explaining its powerful impact.

Dilemmas

Given the success of the PMCCF and SMCCFs, commentators have started arguing that the Fed should be allowed to buy corporate bonds as part of its standard toolkit (link). This might be relevant, but purchases of corporate bonds by central banks raise a number of dilemmas:

- Keeping zombie firms alive. By easing up stresses in corporate bond markets, the Fed calmed down markets. This was the intention of the PMCCF and SMCCF announcements and it worked. It eased access to funding for firms, and firms have raised a lot of cash as a consequence (link). It is positive that malfunctioning markets are stabilized, but if central bank intervention makes markets too cheerful it may allow firms that in principle should not receive funding to nevertheless get it. And, thereby, to keep firms alive for too long, and increase firm leverage too much. Basically, the fear is that programs such as the PMCCF and SMCCFs create too many zombie firms. My CBS colleague Fabrice Tourre and his co-author Nicolas Crouzet has an interesting paper that examines this (link). Fabrice and Nicolas find that when financial markets work perfectly (no disruptions), Fed intervention might be detrimental to economic growth. On the other hand, if markets are disrupted, Fed intervention might prevent a too large wave of liquidations. One thus needs to determine when markets are disrupted “enough” to rationalize interventions in credit markets. This is no straightforward task.

- Distributional aspects. By buying some bonds but not others, the Fed exposes itself to the critique that it helps some firms at the advantage of other. To alleviate such criticism, the Fed has been very transparent and publishes a lot of information about the bonds it buys, the prices at which it buys the bonds, etc. (link). Nevertheless, it is easy to imagine that some firms at some point will start saying ‘Why did you buy the bonds of my competitor, but not my bonds’?

- The Fed put. The more the Fed intervenes when troubles arise, the more investors get reassured that the Fed will also come to the rescue next time around. When the Fed saves markets, it is sometimes called the Fed exercises the “Fed Put”. The potential problem here is that if investors believe that the Fed will exercise the Fed put, investors will be tempted to take on even more risk. Those of us concerned about systemic risks get nervous.

So, in the end, the announcement of the PMCCF and SMCCFs was crucial during this crisis. There are, however, important dilemmas that need to be addressed when evaluating whether such programs should be part of the standard toolbox. I am not saying they should not. I am saying that one needs to be careful.

Conclusion

The Fed launched massive “traditional” interventions in late-February/early March, lowering the Fed Funds Rate and buying mortgage and government bonds. In spite of these very large interventions, equity and credit markets kept on tail spinning. When firms struggle, it hurts economic activity and employment. The Fed got nervous.

The Fed announced – and this is the whole point here; they only announced – that they would start buying corporate bonds. Markets turned upside down. Credit markets stabilized, credit spreads narrowed, corporate bond-market liquidity improved, and stock markets cheered. And, all these things without the Fed spending a single dime until several months after the fact. Even today, the Fed has spent very little (some might say that USD 12bn is a lot, but compared to asset purchases of USD 3,000bn, it pales).

It was a “Whatever it takes” moment. It illustrates how managing investor expectations can be crucial. Understanding this announcement is thus important for understanding the behavior of financial markets during this pandemic.