When oil prices move investors immediately recalibrate their expectations to future inflation rates. This is intriguing. It is also a challenge for central bankers who prefer stable inflation expectations.

In my previous post (link) I analyzed if supply-chain disruptions caused this inflation surge. While preparing the post I stumbled upon an intriguing empirical regularity that I thought would be interesting to analyze further: Expected future inflation is highly correlated with oil prices today. Let me explain.

When oil prices go up, the consumer-price index goes up (keeping everything else constant) because oil consumption is part of total consumption. This increases current inflation. The oil-price increase is not necessarily the underlying reason inflation goes up, as I discussed at length in the previous post (e.g., oil prices might have increased because aggregate demand has increased), but oil prices and inflation rates will naturally always be somewhat corelated.

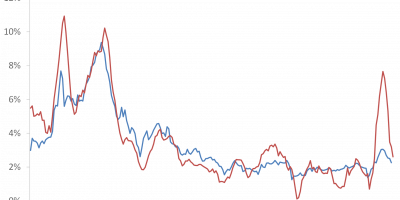

It is more intriguing, but nevertheless true, that oil prices today are correlated with expected future inflation. This appears from Figure 1 that shows how oil prices and expected future euro area inflation (expected rate of inflation over the next two years, two years from now, also called 2y2y inflation expectations) have developed since 2013.

Data source: Datastream via Refinitiv.

Figure 1 reveals a – I would say – surprisingly strong correlation between oil prices and inflation expectations. The correlation is 0.84. If oil prices go up today, investors immediately revise their expectations to future inflation, the figure shows. Similarly, when oil prices fall today, investors immediately lower their expectations to future inflation.

While I can, as mentioned, understand why oil prices today and inflation today are correlated, I find it harder to comprehend why investors immediately revise their expectations to inflation several years down the road when oil prices change today.

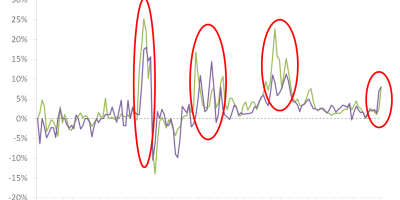

The relationship is even there – albeit slightly weaker (correlation: 0.80) – when we look at expected inflation over the next five years, five years from now, or 5y5y. This is in Figure 2.

Data source: Datastream via Refinitiv.

The effect is also there in the US, though perhaps not as strong as in Europe. Figure 3 shows the relation for the US, for inflation over the next two years, two years from now, 2y2y. The correlation is 0.79. For inflation over the next five years, five years from now (5y5y), the picture basically looks the same and the correlation is 0.72.

Data source: FRED of St. Louis Fed.

Why is this important?

Central banks are concerned about the current rate of inflation, but also about people’s expectations to future inflation rates. If inflation is expected to persist, firms will incorporate this in their price-setting considerations and workers will include it in their wage negotiations. This will make it harder to bring inflation back to target.

Central bankers thus try to influence people’s expectations. When central bank governors say “we will be tough”, they try to convince people that the central bank will deliver on its mandate and bring down inflation, i.e., they try to influence people’s expectations.

Central bankers would also like inflation expectations to remain stable. Alas, they have not. The figures presented here show that inflation expectations move when oil prices move, i.e. inflation expectations have been as volatile as oil prices.

What can explain oil prices’ correlation with inflation expectations?

There is not a great deal of research on this topic, but I am at the same time not the first to wonder why oil prices correlate so strongly with inflation expectations. Relevant papers are here, here, here, here, here, and here, where the latter deals with household expectations, and the other papers with inflation expectations of financial-market investors, either backed out from inflation swaps, as in my graphs above, or from differences between yields on nominal and inflation-protected bonds.

Common underlying factor. The first explanation that comes to mind is that oil prices and inflation expectations are driven by the same underlying factor, such as aggregate demand. When the government pumps trillions of dollars into the economy, aggregate demand goes up. Demand for oil also goes up, pushing up the price of oil today. With a lag, inflationary pressures in the economy build up. Expected future inflation goes up. This makes sense and is probably the best story out there.

The explanation, however, hinges on the assumption that market participants do not believe central banks will fulfill their mandate. If aggregate demand increases, central banks could and should raise interest rates to dampen inflationary pressures. If market participants doubt this will happen, a booming economy might raise both inflation expectations and oil prices, explaining the correlation.

Even if this story makes sense, I doubt it explains it all. First, is the credibility of central banks so low? I don’t think so. Second, oil prices are simply too volatile to be driven by underlying economic activity only, and the moves in expected inflation are similarly too abrupt to be caused by shocks to aggregate demand noly. Hence, other explanations have been proposed.

Risk premia in inflation swaps. In the discussion here I relate oil prices to prices of inflation swaps, implicitly arguing that inflation swaps move because expected inflation moves. While this is a common interpretation in the literature it must be recognized that inflation swaps reflect expected inflation and an inflation risk premium, as I discussed in an earlier analysis (link). This opens the door to another story (entertained for instance here): Oil prices correlate with inflation risk premia but not with expected inflation, explaining why inflation swap rates and oil prices are correlated.

Risk premia reflect the amount of risk and risk aversion. Perhaps inflation uncertainty (the amount of risk) goes up when oil prices go up. The increase in inflation uncertainty then pushes up the inflation risk premium. This is possible, but, again, I am not convinced. It is difficult to imagine why inflation risk should be so correlated with this single factor, that is the oil price. There are so many things that influence inflation, and, thus, inflation uncertainty. Why should inflation risk move so closely with the level of the oil price?

Forward looking asset prices. Oil is a commodity, but is also an asset (people invest in oil), so its price might reflect investors’ expectations. And perhaps falling oil prices reflect an underlying common factor, such as the expectation of weak aggregate demand, pushing down inflation expectations. For instance, this paper (link) argues that the correlation between oil prices and inflation expectations weakens when controlling for stock prices. Stock prices are forward looking and reflect, inter alia, investors’ expectations to future macroeconomic conditions. So, when the correlation between oil prices and inflation expectations weakens when controlling for stock prices, this might indicate that oil prices and inflation expectations react simultaneously to changes in expected future economic conditions. This explanation is related to the first one on a common underlying factor.

During the period I study here, oil and stock prices have not been correlated, though, meaning this explanation does not seem to be the best one either.

So, we have an intriguing correlation, and we have several potential explanations. Each of them probably holds a grain of truth. At the same time, I am not 100% convinced they provide the perfect explanation, meaning this remains somewhat puzzling, at least to me.

Conclusion

During the past decade inflation expectations have moved in tandem with oil prices.

It is only natural that oil prices and current inflation rates are correlated, but it is somewhat intriguing that oil prices and expectations to inflation rates several years down the road are strongly correlated.

I have discussed potential explanations. They all make sense. At the end of the day, I am not sure they provide the full explanation, though.

The correlation between oil prices and inflation expectations is important, whether we fully understand it or not, because inflation expectations matter for monetary policy. If inflation expectations move when oil prices move, it presents a challenge for central bankers who wish to influence and stabilize inflation expectations.