I compare three recent academic explanations why inflation is high: John Cochrane’s, Ricardo Reis’, and my own. The conclusion as a one-liner: Cochrane believes fiscal policy failed, Reis believes monetary policy failed, and I believe both policies failed.

Inflation is on everybody’s mind. People wonder why inflation is so high and what should be done to stabilize it.

Different people have different views. I explained my own views in my last analysis (link), but I believe we can learn from comparing interpretations of the facts. In this post I compare the recent insightful analyses of John Cochrane and Ricardo Reis to my own.

I start out reviewing each explanation, then I compare them, and finally I discuss policy implications. I focus on Cochrane’s, Reis’, and my own explanations, but along the way I point to additional analyses.

John Cochrane’s explanation why inflation is high

John Cochrane has written a number of interesting blog posts and articles on this hot topic. A recent one that collects it all is here (link), but there are more here (link).

John Cochrane takes care to emphasize that he talks about U.S. inflation. He strongly promotes the argument that U.S. inflation is high because U.S. fiscal policy has been too loose.

John is a firm believer in the Fiscal Theory of the Price Level, having written the authoritative book on the topic (link). He writes: “I start by documenting the fundamental fiscal source of our current inflation (link)”. He continues: “Our government printed up about $3 trillion in extra money, and sent it out as checks. It borrowed another $2 trillion and sent more checks. It was a classic helicopter drop.”

From this statement follows a number of important implications. First, today’s high inflation is not a monetary phenomenon. The money supply increased, yes, and this has led some people to argue that everything is straightforward because we have the good old Quantity Theory of Money: PY = Mv. Some people say: “M increased so P increased, which is inflation” (keeping income Y and velocity v constant). John makes clear this is wrong. Fiscal policy caused the increase in the money supply. “Inflation comes from the vast expansion in the overall amount of government debt. Contrariwise, imagine that the Treasury had sent people shares in a mutual fund backed by Treasury debt, with thereby no direct increase in reserves or M2. Surely that would have had much the same effect.” John provides more details in a forthcoming Journal of Economic Perspectives paper (link).

Second, John does not believe supply-chain challenges caused this inflation. “A supply shock can raise the price of affected goods relative to others, and prices relative to wages. It does not raise all prices and wages together”. And: “A shift in demand from services to goods raises the price of the latter, but lowers the price of the former.”

What about monetary policy? Has the Fed been too slow? John has spent a great deal of effort scrutinizing this. I interpret his views as “The Fed failed a little” but the main culprit remains fiscal policy. He writes “one may fault the Fed for not “normalizing” interest rates more quickly. But this is really just a restatement of the joint fiscal-monetary shock view of what got inflation going.”

John derives nice illustrative models to drive home his points. The crucial question in these models is whether people have rational or adaptive expectations. Assume, as John believes, inflation rises because there is a huge one-time fiscal expansion. This raises prices now, but if people are rational and expect there will be no further shocks, people will expect inflation to return to normal. It will take time because prices are sticky, but eventually inflation will stabilize. In this scenario the Fed has not been too slow, and the Fed need not raise interest rates a lot. No need for 8% interest rates, even with inflation at 8%.

Things are different if expectations are adaptive. Adaptive expectations mean that expectations are formed by observing past inflation. If inflation is high today, people expect inflation to remain high tomorrow. The Fed has to increase interest rates a lot to stabilize expectations. In this scenario, the Fed is far behind the curve.

Are expectations rational or adaptive, then? As Cochrane states it: “Rational (or at least consistent) expectations, the idea that people think about the future when making decisions today, has been the cornerstone of macroeconomics since about 1972.”

The Fed is not powerless, even under rational expectations. The Fed can lower inflation in the short run by raising interest rates and causing a recession. Lower inflation in the short run comes at the cost of higher inflation later on, though, John argues. The best way to durably bring down inflation is to coordinate fiscal and monetary stabilizations. Final citation from John (link): “The Fed cannot do it alone. To durably end inflation, the government also has to fix the underlying fiscal problem.”

What about empirical evidence? I find the analysis from San Francisco Fed economists Jordá et al. intuitive and enlightening (link). They show that the CARES Act, signed into law on March 27, 2020, and the American Rescue Plan (ARP) Act of 2021, signed about a year later, boosted real disposable income in the U.S. Jordá et al. use a Phillips curve framework to estimate how disposable income affects inflation. They then simulate a counterfactual scenario where disposable income does not increase. Their main result is copied into Figure 1 below. The green line in Figure 1 is inflation in the U.S. while the blue line shows how inflation counterfactually would have developed if fiscal policy had not been expansionary. Bottom line: Fiscal policy contributed significantly to raising U.S. inflation.

Data source: Figure copied from Jordá et al. (link).

Ricardo Reis’ explanation

Ricardo Reis recently distributed a subsequently much-cited analysis (link). He focuses on the Fed and the ECB “although the points apply more broadly to other central banks in advanced economies”. His conclusion is clear: “Central banks failed to prevent a burst of high inflation in 2021-22”.

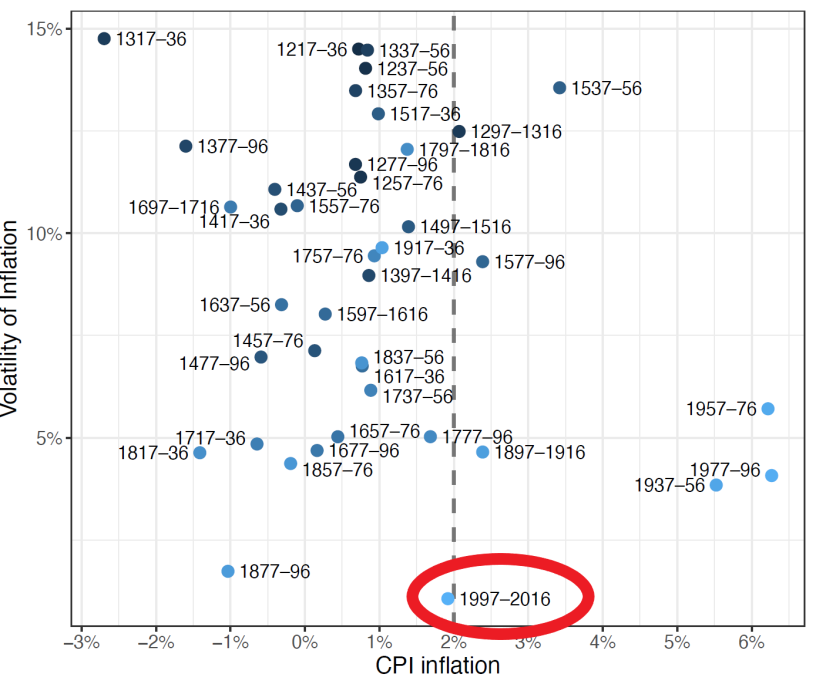

Ricardo starts out emphasizing that central banks have been doing an amazing job throughout the past two decades, up until 2021. He has this great graph, which I copy as Figure 2, which shows combinations of average inflation rates and inflation volatilities across every 20-year period throughout the past eight centuries, i.e. since 1217(!), in the U.K. During the past 20 years, average inflation has been right on target at 2% and inflation volatility has been historically low. I indicate this by a fat red circle in Figure 2. Inflation targeting worked.

Data source: Figure copied from Reis (link).

Today inflation is at 10%, vastly exceeding target. What went wrong?

First, according to Ricardo, central banks misread the nature of the shocks hitting the economy during 2020 and 2021. The first shock was the pandemic. This caused a severe, but short, recession, which was soon after followed by a strong rebound with a strong uptick in demand. Second, supply chains were impaired following and during the pandemic. Third, energy prices rose. Central banks argued that the shocks were temporary, so monetary policy was kept loose. Ricardo writes: “Three times in a row, this diagnosis was plausibly right but disputable, and the risk was that inflation would rise too much and too persistently. After the fact, in all three cases this risk became reality.”

The second mistake was that central banks misread developments in inflation expectations, in particular the probability distributions of expectations. The averages of inflation expectations stayed subdued for relatively long, causing central bankers to argue that inflation expectations remained anchored, whereas in fact the distribution shifted. More and more people became worried that future inflation would be very high. The right-hand tail of the distribution moved, even if the means moved only a little.

Third, central banks relied too much on their credibility. They hoped people would trust them, such that expectations would not move, even if monetary policy was not altered. Instead, people became worried when central banks did nothing in spite of very high inflation. People lost trust in central banks.

Finally, central banks had become convinced that “r-star” (the real interest rate that keeps economic output at its potential) had fallen during recent decades, causing central banks to be more worried about deflation than inflation. Allowing some inflation was thus seen as a good thing. Ricardo expresses doubt that r-star has in fact fallen as much as is typically assumed.

My explanation

In my previous post I presented my explanation of why inflation is so high (link). I will thus keep this review of my own explanation very short and refer to my previous post for the full explanation. I wrote: “I believe there are four main reasons:

- Leaving the pandemic, demand soared.

- Demand was stimulated by too expansionary monetary and fiscal policies.

- Demand shifted, from services to goods. At the same time supply chains were disrupted.

- Commodity prices rose.”

After this review of three economists’ explanations, let me turn to comparisons.

One or several causes

John emphasizes one major cause. Ricardo emphasizes another major cause. I point to several causes.

John believes inflation is high because fiscal policy was too loose. John devotes a lot of attention to carefully examine how central banks should react, but the root cause of this inflation, John argues, is that fiscal policy failed.

Ricardo, on the other hand, believes inflation is high because monetary policy was too loose. The fundamental problem, Ricardo writes, is that “the central bank allowed it (inflation) to rise.”

So, John and Ricardo point to one underlying root cause. They do not point to the same root cause, though. John points to fiscal policy, Ricardo to monetary policy.

I hesitate to point my finger squarely at one policy mistake. I have argued that monetary has been much too expansionary during 2021 and the first half of this year, but I also believe that fiscal policy was too expansionary, in particular in the U.S. I find that both fiscal and monetary policies failed.

On the role of monetary policy

The second – related – difference relates to the role of monetary policy. As to the question whether central banks were too aggressive for too long, John says “it depends”. John’s analyses have been instrumental for clarifying the role of expectations. John finds that if expectations are adaptive, the Fed is behind the curve but if expectations are rational, and inflation is caused by a one-time fiscal policy shock, the Fed is not necessarily behind the curve. Given that the evidence speaks in favor of rational expectations, I read John’s analyses as saying that the Fed did not fail on a grand scale.

Ricardo and I, on the other hand, are very critical towards the, in our view, delayed responses of central banks. As explained above, the whole point of Ricardo’s analysis is that central banks have been too slow because they misinterpreted the shocks hitting the economy. Similarly, I have argued many times that ECB is miles behind the curve (link, link). I thus agree with Ricardo, who states it nicely: “When it (the central bank) allows inflation to deviate significantly from target in the short run, it is by choice, in trading-off other objectives.”

On the role of fiscal/monetary policy coordination

John argues the Fed will face an uphill battle if it–on its own–should be responsible for bringing down inflation (link). Fiscal and monetary policy must be coordinated to promote successful and long-lasting disinflation (link).

While John puts more weight on fiscal policy than Ricardo and I (also because John focuses on U.S. inflation while Ricardo and I want to include a European perspective), I have–similar to John–repeatedly argued that fiscal policy can make monetary policy impotent. My point is that Italy’s debt burden makes it hard for ECB to conduct the right monetary policy (link). In my opinion, ECB assigns too much weight to political goals in its reaction function (that is, keeping Italy’s interest expenses low by preventing yields on Italian sovereign bonds from increasing “too much”). It should assign a higher weight to its main mandate, which is to keep inflation stable. We come from different angles, John from the Fiscal Theory of the Price Level, I from analyzing the ECB, but we agree that too loose fiscal policy can make life difficult for central bankers.

Ricardo does not discuss this but I think he would agree.

On the role of supply-chain challenges

Ricardo and I argue that supply-chain challenges were important. John disagrees.

John argues that an oil price shock increases the price of oil, but that does not necessarily raise other prices, i.e. it is a change in relative prices, not overall inflation. The same goes for important goods. John writes: “My point is just that the obvious story—it’s hard to import chips so the price of chips goes up, causing inflation—is wrong.”

I agree that if nothing else happens (than oil/chips prices going up), it remains a change in relative prices. My point is that many of these goods are not final but intermediate. Oil is used in the production process, chips are used in the production process, so when these prices increase, firms face higher costs of production. As a consequence, firms raise their own prices, thereby causing inflation. A recent paper by Ball and co-authors backs up this interpretation (link). Also, research from the New York Fed (that I will return to below) indicates that global supply factors affect inflation in the euro area and the U.S. (link).

On the role of inflation expectations

Ricardo argues that central banks misread developments in inflation expectations because central banks focused on the means of the probability distributions, which was stable in the beginning, whereas they should have paid more attention to shifts in the tails of the distribution. Even if I have not included this as one of my four main arguments, I agree. I had this analysis (link) that largely made the same point.

John does not discuss changes in the probability distributions of inflation expectations, but my guess is he agrees.

On the role of the war in Ukraine

This can be short. None of us believe the war in Ukraine is the underlying reason why we face so high inflation, simply because inflation started rising long before this terrible war. I presented the evidence in Figure 2 in my analysis (link). John and Ricardo do not even discuss it, i.e. they and I agree that other factors are more important when it comes to what caused this inflation.

Policy implications

John, Ricardo, and I all agree that monetary policy can lower inflation (though, as mentioned, John believes monetary policy can bring down inflation in the short run only, if fiscal policy remains loose). This means central banks must raise policy rates further to bring down this inflation.

John and I agree that too expansionary fiscal policies make life difficult for central bankers. The policy implication is clear: We need to fix the public debt challenges if monetary policy should be able to work as intended. This (fixing the public debt problem) is unfortunately easier said than done.

Ricardo and I agree, while John disagrees, that supply-chain challenges, and the resulting increase in prices of imported goods, contribute to overall inflation. As long as supply-chain frictions remain, this puts upward pressure on inflation, I argue. What do the data say about the current situation?

Supply chains are improving, compared to a year ago, Figure 3 shows. This is good news. However, supply-chain pressures are still elevated. The problem is that it is difficult for central banks and governments to fix supply chains. Central banks can affect demand. If supply is impaired, the pressure for bringing down demand is more pronounced, i.e. also this calls for raising rates.

Other economists

I compare my views to those of John Cochrane and Ricardo Reis, as this (I hope) leads to clear comparisons and policy implications. There are, of course, many other economists who have analyzed the current inflation situation. While I cannot do justice to all of them, let me at least point to some of the more important ones.

Lawrence Summers was first to forecast that expansionary U.S. fiscal policies would lead to inflation in the U.S., so he got the credit (link). Subsequently, Summers and coauthors have produced important research on the tightness of the U.S. labor market and its consequences for inflation (link, link).

Following up on this, I have not discussed the tightness of the U.S. labor market in this analysis, even when it arguably is one of the hot topics these days, because it will determine how much the Fed will have to tighten, and how big the recession in the U.S. will have to be, to bring U.S. inflation back to target. The reason I have not focused on this until now is that while it is indeed an important issue in the U.S., it is not so much (yet) from a European perspective, and I would like to include that.

My reading of the “tightness of the U.S. labor market and monetary policy” analyses is that many economists expect the Fed will have a hard time engineering a soft landing. I agree.

There was this important, though somewhat heated, debate between Blanchard, Domash & Summers and Fed economists during summer. Blanchard et al. argued that unemployment must increase significantly to create enough slack in the labor market (link) while the Fed’s Figura and Waller argued a soft landing is possible (link). That debate centers around the slope of the “Beveridge curve”. The Beveridge curve is the relationship between vacancies and unemployment: Can you generate a significant decrease in vacancies without a large increase in unemployment? Blanchard & Summers say “no”. The Fed (Figura & Waller) says “yes”. Ball et al. (link) has important recent research on this topic.

Finally, regarding central banks’ failure to foresee and prevent inflation, I point to Reis’ analysis. Other people, for instance, White (former BIS official), Wheeler, and Wilkinson have made similar points (link). William writes: “Central bankers have fundamentally misread the nature of the system they are trying to control”.

Conclusion

I presented my views on inflation in my previous analysis (link). I believe, though, we can learn from comparing and contrasting views. Understanding where economists agree and disagree is important for understanding the root causes of inflation and the right policy responses.

I compare my analysis to John Cochrane’s and Ricardo Reis’ thoughtful analyses. We agree on most things, for instance that monetary policy can bring down inflation, fiscal policy contributed to raising inflation, and the war in Ukraine is not the main reason we have inflation.

Not all our views are perfectly correlated, though. For instance, John and I emphasize that fiscal policy excesses make life difficult for central bankers, while Ricardo and I argue supply-chain challenges contributed to this inflation, central bankers misread the persistence of inflation, and, as a consequence, central bankers were too slow to react.